Past CFO Commentary

The commentary in this section speaks only as of the date specified below. The company makes no commitment to update any of this information.

August 14, 2018

As we announced in our second quarter earnings release, we crossed the $250 billion asset threshold1 for heightened regulatory requirements, ending the period at $262 billion in consolidated assets. While we don't believe the consequences will be disruptive to our business model or our strategy, I wanted to share a brief overview of what crossing this threshold means to Schwab and how we have been preparing over the last few years.

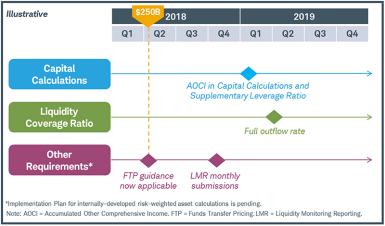

Beginning in 2016, we engaged consultants to review our readiness and help create a roadmap for the increased regulatory requirements. Below is a timeline of the anticipated milestones.

We have grouped the implications into three main work streams: the inclusion of accumulated other comprehensive income (AOCI) in our capital ratios, the increased requirements for the liquidity coverage ratio, and other regulatory requirements and expectations. Assuming we stay above $250 billion in consolidated assets for the remainder of the year, the first significant deadlines for these requirements are in 2019.

AOCI in capital

Historically, we have elected to exclude AOCI, or the net unrealized gains or losses on available-for-sale (AFS) securities, from our calculation of regulatory capital. Starting in 2019, this exclusion is no longer available to us and we are required to include AOCI in our regulatory capital. This means that as the market price of our AFS securities fluctuates, unrealized gains or losses will impact AOCI, and therefore our regulatory capital and ratios. To mitigate this impact, during the first quarter of 2017 we transferred $25 billion of AFS securities to held-to-maturity (HTM), where market fluctuations do not affect AOCI. Furthermore, as we purchase new securities, we are designating more of them as HTM. We intend to bring the size of our AFS portfolio closer to a floor of 20% of total bank assets, thereby balancing liquidity needs with the AOCI impact. Note that we have not made any changes to the composition of the consolidated investment portfolio or interest rate and credit risk profiles. We believe our efforts will keep our current Asset/Liability Management strategy intact while minimizing capital volatility.

Liquidity coverage ratio

In April 2019, we will also be required to adhere to higher standards for our liquidity coverage ratio. This ratio measures our amount of high-quality liquidity assets (HQLA) divided by the amount of our prescribed outflows, an indication of our ability to withstand a short-term liquidity event. Currently, we are required to measure 70% of prescribed outflows in the denominator. By crossing $250B in consolidated assets, we will soon be required to measure 100% of prescribed outflows. We are strategically adding more Level 1 securities (Ginnie Mae mortgage-backed securities, U.S. Treasuries, and Excess Reserves) in our investment portfolios to increase our HQLA to meet the increased liquidity coverage ratio requirements. As we seek the optimal mix of Level 1 securities, near-term improvement in our net interest margin (NIM) may be impacted, yet we still believe the long-term effect of these purchases will be small—about one basis point of NIM. We'll also be required to calculate this ratio on a daily basis, but we are already prepared to do so.

Other regulatory requirements and expectations

Lastly, we will be held to a range of higher regulatory standards and expectations, including:

- Additional governance, risk management, reporting, and capital requirements.

- Funds Transfer Pricing.

- Liquidity Monitoring Reporting.

- Implementation Plan for internally-developed risk-weighted asset calculations.

In preparation, we've hired staff in the risk management and regulatory areas. We also continue to invest in enhancing our automation and systems to improve efficiency and meet reporting requirements. These costs are largely in our run rate and we do not anticipate a significant step-up in expenses going forward.

As Schwab continues to grow, maintaining a healthy balance sheet is essential. By proactively addressing these heightened regulatory requirements, we will be ready to respond to the evolving landscape while continuing to serve clients seamlessly into the future.

1. The $250 billion consolidated asset threshold is triggered when assets are greater than $250 billion at year-end.

Forward-looking statements

This commentary contains forward-looking statements relating to: the consequences of crossing and remaining above the $250 billion consolidated asset threshold; deadlines; size of our AFS portfolio; our asset/liability management strategy; capital volatility; adding Level 1 securities to meet increased liquidity coverage ratio requirements and the related near-term and long-term impact on our net interest margin; investing in automation and systems to improve efficiency and meet reporting requirements; and expenses.

Important factors that may cause such differences include, but are not limited to, regulatory guidance; general market conditions, including the level of interest rates and securities valuations; competitive pressures on pricing, including deposit rates; the company's ability to enhance automation and systems in a timely and effective manner; the level of client assets, including cash balances; the company's ability to monetize client assets; capital and liquidity needs and management; the company's ability to manage expenses; client sensitivity to rates; and the timing and amount of transfers to bank sweep.