Past CFO Commentary

The commentary in this section speaks only as of the date specified below. The company makes no commitment to update any of this information.

December 14, 2022

Today we published our monthly activity report and supplement for November 2022. The release highlighted the continuation of our strong business momentum as demonstrated by yet another month of over $30 billion in net new assets – representing a November quarter-to-date organic growth rate of approximately 7%. While we look forward to unpacking some of the drivers helping to support our sustained success with clients at the Winter Business Update next month, I wanted to take a moment today to provide some perspective on several notable topics, including total accounts, average interest-earning assets (AIEA), and client cash sorting.

1. Active Brokerage Accounts

Despite recording over 300,000 new account openings in November, total active brokerage accounts declined slightly on a month-over-month basis. The 1% drop was not driven by an uptick in account attrition, but rather the result of recent account “scrubbing” activity. If you would like a refresher on our general approach to this practice, I would encourage you to read my commentary from May 2021.

Our recent scrubbing efforts reflect actions we are taking in advance of the first Ameritrade client conversion scheduled for February. Over the last few months, we have been performing maintenance on Ameritrade accounts with low, non-zero balances and limited activity to prepare for an efficient client transition. Based on these efforts, some clients chose to re-engage with Schwab, resulting in approximately $65 million of incremental net new assets. However, there were still many accounts that took no action. In such cases, we decided to move forward with closing the account. During the past few months, we have scrubbed over 500,000 accounts, representing less than $7 million in assets, including approximately 350,000 accounts during November.

2. Average Interest-earning Assets

We reported November AIEAs of $527 billion, down 5% relative to the prior month. While expected client cash sorting factored into this movement, the decline was primarily driven by our decision to reclassify certain bank portfolio investments as held-to-maturity (HTM). As disclosed in our most recent 10-Q on November 2, we transferred another $80 billion of U.S. agency mortgage-backed securities from the available-for-sale (AFS) category to the HTM category. At that time, these securities had a pre-tax unrealized loss of approximately $16 billion attached to them.

As I said at our Fall Business Update, moving the securities from AFS to HTM reduces the volatility within accumulated other comprehensive income (AOCI) and our tangible common equity (TCE). GAAP accounting rules stipulate that securities classified within HTM are not marked-to-market. Therefore, following the transfer, the fair value of the fixed income investments will not fluctuate based on movements in interest rates – thereby helping to limit future unexpected swings in AOCI as well as TCE.

Upon transferring an AFS security to HTM, any unrealized gains or losses at that time are “crystallized” or factored into the amortized cost of the security1. Therefore, immediately after the reclassification, our interest-earning assets were reduced by the associated unrealized losses – or approximately 3% of the October average balance. As mentioned previously, those crystallized losses will amortize down as the securities mature – with one-third of the unrealized losses accreting back to stockholders’ equity within approximately 24 months.

It is important to emphasize that this transfer has no impact on net interest revenue as the economic profile of the underlying securities remains unchanged. We are now expecting 4Q22 NIM to approach the mid 220s basis point range – versus the mid 210s I referenced during the Fall Business Update back in October.

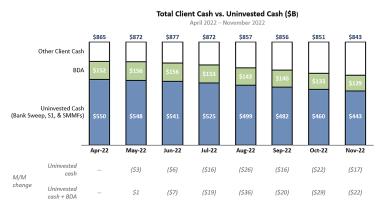

3. Client Cash Balances and Sorting Activity

As markets rebounded and clients continued to engage across both equity and fixed income investments, total client cash declined by $8 billion from the prior month to end November at $843 billion, or 11.5% of total client assets.

The combination of this client investment activity and anticipated cash sorting pushed uninvested cash (ex-Bank Deposit Account balances) down by $17 billion versus October. This decline included a $12 billion drawdown in bank sweep deposits – the smallest month-over-month change since July:

Note: Certain totals may not sum due to rounding. S1 = Schwab One® and other broker-dealer free credits. SMMFs = Sweep money market funds. BDA = Bank Deposit Account. Uninvested cash = Bank sweep deposits, Schwab One®, and SMMFs.

The incremental decline in balance sheet cash beyond bank sweep was primarily attributable to a drop in non-interest-bearing credits and unsettled funds from a temporarily elevated level at the end of October. These amounts are directly tied to client trading activity and therefore can vary depending on what is still awaiting trade settlement as we close the books on the last day of the month.

Overall year-to-date client cash sorting remains in-line with our expectations, and we believe December 2022 AIEA will be down 13% to 15% on a year-over-year basis – consistent with our prior outlook when adjusting for the impact of the aforementioned HTM transfer.

1 Interest-earning assets, including both AFS and HTM securities, are presented on an amortized cost basis.

Forward-Looking Statements

This commentary contains forward-looking statements relating to Schwab’s business momentum and client success; net interest margin; client cash sorting; and average interest-earning assets. These forward-looking statements reflect management’s expectations as of the date hereof. Achievement of these expectations and objectives is subject to risks and uncertainties that could cause actual results to differ materially from the expressed expectations.

Important factors that may cause such differences include, but are not limited to, the company’s ability to attract and retain clients and independent investment advisors and grow those relationships and client assets; develop and launch new and enhanced products, services, and capabilities, as well as enhance its infrastructure and capacity, in a timely and successful manner; hire and retain talent; support client activity levels; successfully implement integration strategies and plans; manage expenses; and monetize client assets. Other important factors include client use of the company’s advisory solutions and other products and services; general market conditions, including the level of interest rates and equity valuations; client cash allocation decisions; client sensitivity to rates; competitive pressures on pricing; level of client assets, including cash balances; capital and liquidity needs and management; balance sheet positioning relative to changes in interest rates; interest earning asset mix and growth; the level and mix of client trading activity; market volatility; margin loan balances; securities lending; the migration of bank deposit account balances; and other factors set forth in the company’s most recent reports on Form 10-K and Form 10-Q.