Past CFO Commentary

The commentary in this section speaks only as of the date specified below. The company makes no commitment to update any of this information.

January 18, 2023

This morning’s earnings release highlighted the power of Schwab’s consistent strategy, as our focus on meeting the needs of individual investors and the advisors who serve them helped drive continued business momentum. While equity and bond markets suffered their worst year since 2008, clients turned to us for help. During 2022, they entrusted us with over $425 billion in net new assets, an amount which was impacted by record tax-related outflows in April. We ended the year on a high note, gathering $128 billion of net new assets in the fourth quarter alone – representing an annualized organic growth rate of approximately 8%. With the help of higher rates, we converted this sustained success with clients into record full-year financial results – GAAP earnings per share of $3.50 or $3.90 on an adjusted basis(1).

While these results speak for themselves, I thought it might be helpful to call out a few items included within today’s release as well as spend a moment on Bank Deposit Account (BDA) revenue and cash sorting.

Other revenue came in at $174 million for 4Q22, down 5% relative to the third quarter. The primary driver for the sequential change was an incremental provision for credit loss of approximately $25 million driven by the response of our model-based methodology to the combination of forecasted declines in U.S. home prices and higher interest rates. I want to emphasize that there has been no noticeable change in delinquencies or current payment trends in Schwab’s loan book. The increased reserve was entirely based on current and forecasted trends across the broader economy. During recent cycles, as macroeconomic conditions rebounded, we have been able to release credit reserves – and in some instances end up in a net recovery position.

For the BDA revenue line, given that we continue to get a fair number of questions regarding this item, we thought it would be helpful to revisit certain mechanics as well as reiterate where you can find supplemental information. While the details of this arrangement are fairly intricate, the financial drivers are reasonably straightforward. For the purposes of this commentary, I am going to focus solely on the Insured Deposit Account (IDA) balances that are held at two North American subsidiaries of The Toronto-Dominion Bank (TD). These IDA balances represent over 95% of the total balances within the BDA structure as of December 31, 2022. As a reminder, we provide updated balance information on a quarterly basis within the appendix of our business update materials as well as monthly data via the SMART Supplement. Both documents are available on the Financial Reports & Presentations page of the Schwab Investor Relations website.

Note: BDA = Bank deposit account. IDA = Insured deposit account.

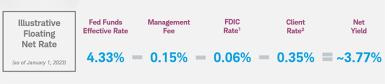

We also provide data regarding the net rate earned by Schwab on both floating and fixed balances within the aforementioned quarterly business update materials. The net rate is a function of gross yields less applicable costs. Using floating balances as an example, the gross yield is based on the Fed Funds Effective Rate. You then need to subtract the TD management fee, applicable FDIC fees, and the current rate paid to clients. The cash solutions page on the Ameritrade website is the best source to track the rate paid on clients’ transactional cash sitting within the BDA. To further the example, here is a build-up of the net rate on floating IDA balances as of January 2023:

Note: FDIC = Federal Deposit Insurance Corporation. 1. FDIC rate increase to approximately 6 basis points went into effect on January 1, 2023. 2. Ameritrade client rate paid on transactional cash balances increased by 5 basis points to 35 basis points effective January 1, 2023.

Note: FDIC = Federal Deposit Insurance Corporation. Source for FF Effective: Effective Federal Funds Rate - FEDERAL RESERVE BANK of NEW YORK (newyorkfed.org)

Finally, I’d be remiss to not at least mention client cash sorting. Activity through year-end continued to trend in-line with our expectations, as December 2022 average interest-earning assets equaled $520 billion – a 14% decline from the prior December average or the midpoint of the 13% – 15% range provided in my previous commentary published last month. Additionally, end of period interest-earning assets also closed the year at $520 billion.

At the upcoming Winter Business Update scheduled for January 27, we look forward to sharing additional empirical data and insights regarding client sorting behavior and quantitative analysis around this topic. These analyses bolster our confidence that we’re entering the later innings (though not the last inning) of the cycle and that net sorting activity should abate at some point during 2023.

(1) Further details on non-GAAP financial measures and a reconciliation of such measures to GAAP reported results can be found on pages 11–12 of our earnings release dated January 18, 2023.