Past CFO Commentary

The commentary in this section speaks only as of the date specified below. The company makes no commitment to update any of this information.

May 5, 2023

As we have done in the past, we wanted to use this forum to provide you with an update on a couple of topics – a Second Amended and Restated Insured Deposit Account Agreement (2023 IDA) and the noticeable slowing in client cash allocation activity we have experienced over recent months.

In our 8-K filing today, we announced that we and TD Bank, N.A. and TD Bank USA, N.A. (collectively “TD Bank”) have entered into the 2023 IDA which extends the agreement until July 1, 2034. Schwab and TD Bank have agreed to this extension and other modifications to the Amended and Restated Insured Deposit Account Agreement from late 2019 (2019 IDA) in order to allocate the impact of changing market conditions with greater clarity and in a mutually agreeable way. I’d like to briefly explain the key changes and what it means moving forward:

- Those of you familiar with the 2019 IDA will recall that balances in the IDA are either fixed – meaning the yields were set at a specified yield for a specified period of time – or floating. The fixed balances, officially known as Fixed Rate Obligation Amounts (FROAs), decrease over time as they “mature”. Per the new 2023 IDA, Schwab must maintain total balances above the level of FROAs, and we have the option to “buy down” up to $5 billion of FROAs balances by paying a market-based fee.

- The 2019 IDA required Schwab to ensure that at least 80% of total balances are fixed. This amendment eliminates that requirement.

- In addition, the 2019 IDA set a floor for total IDA balances at $50 billion. That floor has now increased to $60 billion, with the corresponding addition of a cap on the total amount of balances in the IDA that is $30 billion above the applicable floor (initially the total level of FROAs, and then starting in September 2025 the new floor of $60 billion).

Our ability to eventually have 100% floating rate balances provides several long-term benefits, notably the increased capital and liquidity efficiency given the typical yield differential between what we receive on those balances under the agreement versus what we can earn investing in floating rate securities ourselves – especially when factoring in the cost of capital. Said another way, using the 2023 IDA to help manage some of the ebbs and flows of client cash balances can create more stability within Schwab’s on-balance sheet deposit base AND boost our return on equity.

While the 2023 IDA provides further clarity and helps maintain operational and financial flexibility going forward, it also sets the stage for an enhanced experience for our clients as we continue to provide them with a leading banking experience as part of our modern wealth management offering.

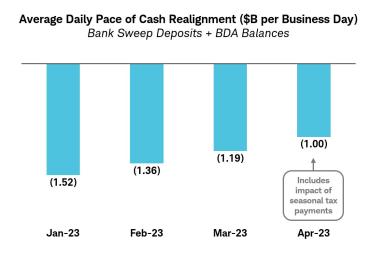

With regard to client cash allocation activity, the favorable month-to-date trajectory highlighted at the recent Spring Business Update persisted through the end of April – as the pace of outflows slowed during what is historically a stronger outflow month due to tax payments:

This steadily improving trend marks the third consecutive month of observed deceleration in the daily average pace of cash realignment within bank sweep and Bank Deposit Account (BDA) balances – further bolstering our conviction in this activity abating during 2023 and a resumption in growth of client cash on the balance sheet.

As mentioned previously, this client cash realignment is something we have been helping our clients do for over a year. The balances are staying at Schwab and they are being redeployed by clients into other products across the firm to help them meet their financial goals. While Bank Sweep Deposits plus BDA balances are down $104 billion year-to-date, select yield products (including certificates of deposit, purchased money market funds, and fixed income securities) have increased by $194 billion over the same period.

The combination of these trends – along with robust year-to-date organic growth and a 6th consecutive month of over 300 thousand new brokerage accounts – demonstrates the strength of our client-centric model which positions us to deliver attractive ‘through the cycle’ returns for stockholders.

Forward-Looking Statements

This commentary contains forward-looking statements relating to the benefits of the 2023 IDA, including capital and liquidity efficiency, balance sheet deposit base stability, and return on equity; operational and financial flexibility; client experience; client cash realignment activity and trends; growth of client cash on the balance sheet; and stockholder returns. These forward-looking statements reflect management’s expectations as of the date hereof. Achievement of these expectations and objectives is subject to risks and uncertainties that could cause actual results to differ materially from the expressed expectations.

Important factors that may cause such differences include, but are not limited to, general market conditions, including the level of interest rates and equity valuations; client cash decisions; client sensitivity to rates; level of client assets, including cash balances; competitive pressures on pricing; capital and liquidity needs and management; balance sheet positioning relative to changes in interest rates; interest earning asset mix and growth; new or changed legislation, regulation or regulatory expectations; client use of the company’s advisory solutions and other products and services; the level and mix of client trading activity; market volatility; margin loan balances; and securities lending. Other important factors include the company’s ability to attract and retain clients and independent investment advisors and grow those relationships and client assets; develop and launch new and enhanced products, services, and capabilities, as well as enhance its infrastructure and capacity, in a timely and successful manner; hire and retain talent; support client activity levels; successfully implement Ameritrade integration strategies and plans and achieve expected cost synergies; monetize client assets; manage expenses; and other factors set forth in the company’s most recent reports on Form 10-K and Form 10-Q.