401(k) Participants' Investing Behavior May Leave Them Short

Two-thirds of participants view themselves as savers, not investors

New research from Schwab Retirement Plan Services finds that although 401(k) participants believe they need $1.7 million, on average, to retire, many are not investing enough to reach that goal. The nationwide survey of 1,000 401(k) plan participants also reveals the outsized role of the 401(k) in Americans’ financial lives, with most (58%) saying it is their only or largest source of retirement savings.

Moreover, two-thirds (65%) of those surveyed say participating in a 401(k) plan was their first experience with investing – yet when it comes to using a 401(k), 64 percent view themselves as savers rather than investors. In fact, the survey shows that outside of a 401(k), participants are more likely to use a savings account to prepare for retirement than any type of investment account.

Steve Anderson quote

“The people we surveyed have a realistic target for retirement, but many likely aren’t on track to get where they want to go. It’s important for anyone with a 401(k) plan to understand that they’re already an investor, whether they realize it or not,” said Steve Anderson, president, Schwab Retirement Plan Services.

Shifting your mindset from ‘saving for retirement’ towards ‘investing for retirement’ can help you to better understand that you are participating in the market when you contribute to a 401(k), and ultimately better help you reach your goals.”

Steve Anderson

President, Schwab Retirement Plan Services

Missed investment opportunities

While everyone’s path to retirement is different, investing a sufficient percentage of your salary early on is key to growing a nest egg. Half of those surveyed (51%) are contributing 10 percent or less of their salary to their 401(k), with the average annual contribution totaling $8,788. This is a good start but may not be enough, especially if you start investing for retirement later in life. To put this in perspective, Schwab has determined that if you start in your 20s, you will likely be able to retire comfortably by investing 10 to 15 percent of your salary each year. But if you don’t start until age 45 or older, you might need to invest as much as 35 percent of your salary annually, which would be a significant challenge for most workers.

And when asked how they decided how much to contribute to their plan initially, 55 percent say they chose a percentage they were comfortable with, 36 percent contributed as much as their employer matched and 8 percent were automatically enrolled at a default percentage chosen by their employer. Among those surveyed who were auto-enrolled into their 401(k) plan, 33 percent have never increased their contribution rate and 44 percent have never changed their investment choices.

“Any effort to set aside money for the future is worthwhile. That said, money intended for retirement has far more growth potential if it’s invested through an IRA or Health Savings Account, for example, than if it’s placed in a regular savings account,” added Catherine Golladay, chief operating officer at Schwab Retirement Plan Services. “Having access to more investment education could help participants get more out of their investments, both inside and beyond their 401(k) accounts.”

Opportunities for education

With workplace retirement plans playing such a vital role in Americans’ financial preparations, employers have an opportunity to offer tools and resources to foster workers’ financial wellbeing, including access to advice and managed account services.

Nearly all of those surveyed (95%) acknowledge they would feel confident in making the right financial decisions with professional help, yet just half of participants (52%) feel their situation actually warrants financial advice.

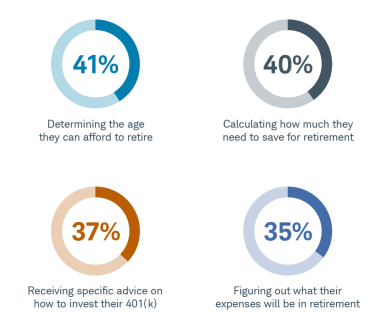

Survey participants named some of the specific areas where they would like help, including:

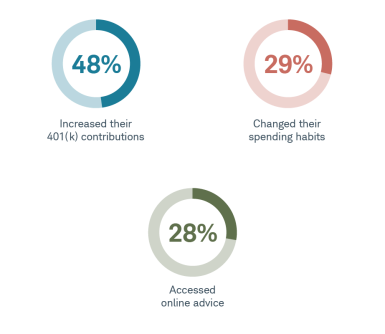

Many participants leverage and find value in web-based financial tools, with just over half (52%) saying they have used an online retirement calculator. Of those who have used one, 71 percent felt encouraged and wanted to learn more, and 61 percent even took positive actions related to their finances.

Actions taken by participants after using an online retirement calculator.

“It’s so encouraging to see people using online resources to take their financial pulse, and even more encouraging that many are taking action. The next step would be talking with a financial professional, a service many people can access through their 401(k),” added Golladay. “We believe everyone can benefit from professional financial advice, and by offering it at work, employers can help move their employees from saving to investing to true financial ownership.”

Other notable survey findings

Must-have benefits.

The vast majority of participants (87%) consider a 401(k) a must-have benefit. Only health insurance ranked higher (89%).

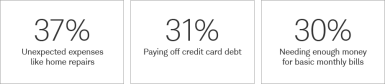

Top obstacles participants face.

Participants named unexpected expenses as the top obstacle they face when trying to save for retirement. Just fourteen percent named paying off student loans as an obstacle. The top obstacles named include:

Sources of financial stress

Similarly, participants' top sources of financial stress are:

401(k) loans.

Finally, a quarter (26%) of participants have taken a loan from their 401(k). Of those, more than half have taken multiple loans.

About the survey

This online survey of U.S. 401(k) participants was conducted by Logica Research for Schwab Retirement Plan Services, Inc. Logica Research is neither affiliated with, nor employed by, Schwab Retirement Plan Services, Inc. The survey is based on 1,000 interviews and has a 3 percent margin of error at the 95 percent confidence level. Survey respondents worked for companies with at least 25 employees, were current contributors to their 401(k) plans and were 25-70 years old. Survey respondents were not asked to indicate whether they had 401(k) accounts with Schwab Retirement Plan Services, Inc. All data is self-reported by study participants and is not verified or validated. Respondents participated in the study between March 19 and March 29, 2019. Detailed results can be found here.

About Charles Schwab

At Charles Schwab we believe in the power of investing to help individuals create a better tomorrow. We have a history of challenging the status quo in our industry, innovating in ways that benefit investors and the advisors and employers who serve them, and championing our clients’ goals with passion and integrity.

More information is available at www.aboutschwab.com. Follow us on Twitter, Facebook, YouTube and LinkedIn.

Financial tools and resources are available at www.schwabmoneywise.com.

Through its operating subsidiaries, The Charles Schwab Corporation (NYSE: SCHW) provides a full range of securities brokerage, banking, money management and financial advisory services to individual investors and independent investment advisors. Its broker-dealer subsidiary, Charles Schwab & Co., Inc. (member SIPC, www.sipc.org), and affiliates offer a complete range of investment services and products including an extensive selection of mutual funds; financial planning and investment advice; retirement plan and equity compensation plan services; compliance and trade monitoring solutions; referrals to independent fee-based investment advisors; and custodial, operational and trading support for independent, fee-based investment advisors through Schwab Advisor Services. Its banking subsidiary, Charles Schwab Bank (member FDIC and an Equal Housing Lender), provides banking and lending services and products. More information is available at www.schwab.com and www.aboutschwab.com.

The Charles Schwab Corporation provides services to retirement and other benefit plans and participants through its separate but affiliated companies and subsidiaries: Charles Schwab Bank; Charles Schwab & Co., Inc.; and Schwab Retirement Plan Services, Inc. Trust, custody, and deposit products and services are available through Charles Schwab Bank. Schwab Retirement Plan Services, Inc. is not a fiduciary to retirement plans or participants and only provides recordkeeping and related services.

Schwab MoneyWise® is provided by Charles Schwab & Co., Inc.

©2019 Schwab Retirement Plan Services, Inc. All rights reserved.